Get Started

Seeking and maintaining employment as a MilSpouse can be challenging. We’ve got tips, considerations and resources whether you work for yourself or someone else.

Get Started Now

Financial Planning

Earning additional income for your family is rewarding. We dive into the details to help you enhance your family’s financial plan to reach your goals.

Financial Planning Considerations

Resources

Learn about the resources available within the military community. There are sources of support and information available online and at the installation.

Know What's Available

1

Get Started

Have a boss? Or want to be the boss?

As a multifaceted military spouse, employment or entrepreneurship offers more than just money. Common motivations include:

- Greater financial security

- Personal satisfaction

- Increased independence

- Social and intellectual engagement

- Foundation for future opportunities

Every spouse with a job, career or business of their own has their unique reasons for doing it. What’s most important is that you understand your motivation, because military spouse employment can present a unique set of challenges. Having a clear sense of purpose can help you overcome those challenges when they arise.

As you think through this, check out these employment-related tips from Caitlin and Thorunn, each a military spouse of over 10 years.

Military-Provided Spouse Employment Resources

Sometimes, the hardest step in pursuing employment as a military spouse is knowing where to start. If that’s you, be sure to get familiar with these resources:

Installation-Based Employment Assistance Programs – Each branch of service has programs on the installation to provide military spouses employment-related tools and support.

| Army | Employment Readiness Program (ERP) |

|---|---|

| Marine Corps | Family Member Employment Assistance Program (FMEAP) |

| Navy | Family Employment Readiness Program (FERP) |

| Air Force/Space Force | Employment Assistance Program |

| Coast Guard | Spouse Employment Assistance Program (SEAP) |

SECO – The Spouse Education and Career Opportunities program is a Department of Defense program designed to “provide education and career guidance to military spouses worldwide, offering comprehensive resources and tools related to career exploration, education, training and licensing, employment readiness and career connections.” The MySECO website is a one-stop shop for all things spouse employment. Create a profile to be searched by MSEP employers, find thousands of employment opportunities or chat directly with a Career Coach.

Said another way, you really should check out this program if you’re a military spouse looking to advance your personal, professional and career opportunities.

SECO Career Center – 800-342-9647. Get your personal certified career coach to assist you in every aspect of reaching your employment goals.

MSEP – The Military Spouse Employment Partnership is “an employment and career partnership, connecting military spouses with hundreds of partner employers who have committed to recruit, hire, promote and retain military spouses.”

The program’s website includes open job opportunities, including a specific search option for telework or remote job opportunities.

Additional Considerations — Have a Boss

In addition to the great information available through the resources listed above, consider these additional tips if working for someone else is your thing:

Additional Considerations — Be the Boss

SECO can also help if calling the shots is more your thing with a Career Coaching Package designed specifically for military spouse entrepreneurs. Here are some additional considerations for entrepreneurs:

2

Financial Planning

Have a Boss

Working for a paycheck can be both financially and emotionally rewarding, but it may also have effects that are not obvious at first. So, before you make that leap from home life to work life, it’s important to look at some additional considerations that can impact both your finances and your family. In addition to increased income, here are some additional things to consider on the expense side.

The old phrase “you have to spend money to make money” can show up in the form of new expenses once you start working. Having a better understanding of these expenses can help you calculate the actual income and cost of that new opportunity. Below are some common work-related expenses that you might need to account for:

Implementing a spending plan can help you make the most of your money and can keep you from overspending. Visit Money Ready – Create a Budget to learn how to build or update your plan. You can also download the spending plan worksheet here to get started.

✓ Insurance Considerations

It is a good idea to review and compare benefits like health and life insurance coverage if your employer offers them in order to maximize benefits and minimize costs.

Health

Service members and their families are eligible for TRICARE health coverage. Your coverage options depend on your status and location. This will be TRICARE Prime or Select for active-duty and certain reserve spouses and family members. It will be TRICARE Reserve Select for other reserve spouses and family members. Visit this resource for more information.

Your civilian employer may also offer you coverage with a variety of plans from which to choose. Be sure to review both plans and select the best option for you and your family. Compare copays, deductibles and coinsurance to check for cost savings. Keep in mind, if you elect your employer health insurance plan, it may become your primary coverage and TRICARE will become secondary. You can learn more about other health insurance and coordination of benefits here.

Life

As a military spouse, you may have coverage under the Family Servicemembers’ Group Life Insurance (FSGLI), which covers a Service member’s spouse up to a maximum of $100,000. Your cost depends on your age, but it’s typically less than $10 per month for most people. You may find that you need additional coverage, and one source for this might be your employer.

Group term life insurance is a common benefit provided by employers. It typically has little, or no underwriting, and coverage is in effect for the period you are employed. Most employers will subsidize the costs for the coverage up to a certain amount. Please note that group policy coverage is not generally portable and will terminate if you leave employment.

It’s worth taking the time to compare your employer-provided coverage with what is available through the military. It’s important to review your life insurance needs and select the right amount of coverage if your family is relying on two incomes. You may find that you need more than what the military and your employer provide. In that case, you may need to supplement with an individual policy.

✓ Retirement Saving Considerations

Participating in an employer-sponsored retirement plan if one is available is one way to boost your retirement savings -- especially, if you haven’t been able to save much toward this goal outside of your spouse’s Thrift Savings Plan (TSP).

Here are some key points to consider:

Learn more about saving for your own retirement, strategies for saving, and the various account options available.

✓ Family Considerations

Combining your work life with family life can pose some challenges. Cooking, cleaning, laundry and grocery trips may now require some discussion and coordination. To achieve a smooth transition, it’s crucial for you and your spouse to come to an agreement on how the household chores need to be divided and managed, especially when it comes to children or pets.

Ensuring you have high-quality child care is not just for your child’s benefit but also for your peace of mind. The good news is the military recognizes the importance of support for military families and provides a wide range of child care and school programs to meet your family’s needs. You can learn more about military child care programs on Military OneSource.

Will your work schedule allow the flexibility to attend family events, school programs and sporting events? Achieving work-life balance can be challenging, but it is possible with some effort, family coordination and a little planning. There’s no need to feel guilty about missing an occasional soccer game or recital. Consider planning for a stand-in like your spouse, parent or in-law to take your place.

Be the Boss

Working for someone else – having a boss – is a great option for many military spouses. But sometimes, working for yourself – being the boss – is better. This is especially true if you start a business that can move with you each time you PCS.

Working for someone else – having a boss – is a great option for many military spouses. But sometimes, working for yourself – being the boss – is better. This is especially true if you start a business that can move with you each time you PCS.

That said, launching a new company will almost certainly require some additional planning. Here are some points to ponder.

✓ Financial Considerations

One of the main differences between working for yourself or someone else is the personal financial commitment you may need to make when striking out on your own. Whether it’s money for building your inventory, paying legal fees or licensing requirements, or any number of other start-up costs, there’s a good chance you’ll need some upfront cash to get your business started. Plus, you may also have to operate your business “in the red” for a while, where your monthly business expenses exceed the business’ income.

Upfront outlays and initial cash flow shortfalls are both normal when starting a business. However, given that short-term cashflow problems are one of the biggest reasons small businesses fail, it’s critically important to try to predict what needs and shortages your business might experience, as well as how long they’ll last. This can help you make sure you either have the funds already in place to cover your needs or have a plan to get the money when necessary.

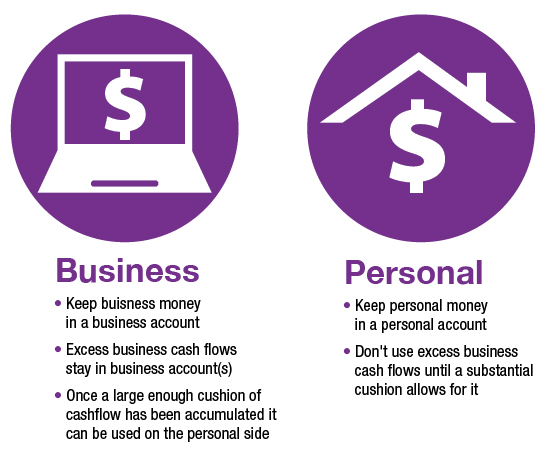

Another important consideration when starting a business is how to separate your personal finances from your business finances. Small business cashflows often ebb and flow, resulting in extra money one day and shortages the next. Depending on your business structure, this can wreak havoc on your personal finances if your business and personal finance worlds are intertwined. To decrease this risk, account for your business money on the business side, and your personal money on the personal side, as much as possible. This typically means maintaining business cash flows in separate business accounts rather than comingling them with personal monies. Then, after establishing a large enough cushion on the business side to meet expenses and handle unexpected costs, excess business net profits may be transferred to personal accounts for personal needs.

Another important consideration when starting a business is how to separate your personal finances from your business finances. Small business cashflows often ebb and flow, resulting in extra money one day and shortages the next. Depending on your business structure, this can wreak havoc on your personal finances if your business and personal finance worlds are intertwined. To decrease this risk, account for your business money on the business side, and your personal money on the personal side, as much as possible. This typically means maintaining business cash flows in separate business accounts rather than comingling them with personal monies. Then, after establishing a large enough cushion on the business side to meet expenses and handle unexpected costs, excess business net profits may be transferred to personal accounts for personal needs.

Here are some planning topics to consider:

✓ Income Tax Considerations

One potentially significant upside of having your own business is the opportunity to benefit from business-related income tax deductions. Small business expense write-offs reduce the taxable income of your business, resulting in you having to pay less tax on revenue generated by it. Some common examples include the potential ability to deduct certain home-office and auto expenses, computer equipment, travel expenses and business meals, just to name a few. It’s important to realize though, that writing off business expenses must be done accurately.

The IRS can, and often does, impose penalties for tax reporting gone wrong. Consequently, if you are deducting car, home office or other items that may overlap with your personal expenses, be sure to read and follow the IRS rules for handling personal vs. business expenses, to include IRS Publication 578, Business Use of Your Home (Including Use by Daycare Providers). Establishing appropriate accounting books and records for your business at the start will assist with your business tax filing activity. The same is true for keeping receipts – whether you think the expense is deductible or not. Better to have a receipt and not need it than need one and not have it.

Tax-filing software with a business module may be helpful to file your taxes. It may be wise to secure the assistance of a professional tax advisor early in your business ownership journey if you are unsure of your tax options and responsibilities. When you are profitable, determine how much of that you should be saving/paying to the IRS early on.

✓ Retirement Saving Considerations

Being the boss means creating another stream of income for yourself and your family. That’s obviously great for the day-to-day expenses we all face, but it also presents an opportunity for a better retirement. With retirement savings being a potentially significant benefit of business ownership, it’s a concept you may want to become more familiar with.

The type of business you have, whether you have employees, and how much you want to set aside are just a few of the main factors in determining which type of retirement plan is best for you, but there are three main types of plans available:

| Plan Type | Potential Options |

|---|---|

| IRA-Based Plans |

|

| Defined Contribution Plans |

|

| Defined Benefit Plans |

|

Tax advisors, who are typically well-versed in small business retirement plans, can often be a great resource to help you decide which retirement plan approach is right for you. The IRS has also made a wealth of information available on the topic including Publication 3998, “Choosing a Retirement Solution for Your Small Business.” In addition to an employer-sponsored retirement plan, you may also contribute to an IRA. Be sure to understand the contribution and deduction limits for your situation.

✓ Family Considerations

No discussion on starting a business would be complete without examining perhaps the most important topic of all: Your family.

The fact is, starting a small business frequently requires a substantial time commitment, financial commitment, or both, which will likely have an impact on your family. The extent of that impact will really depend on your specific situation and family dynamics but exactly how your business will affect your family could warrant some serious thought, collaboration with your spouse and possible planning.

For instance, it could be important to plan for the following:

- Family dynamic changes – division of household labor

- Longer working hours

- Potential for missed family or children’s events

- Increased stress

- Interrupted vacations

- Potentially tight household finances

- Child care needs

While this is a list is of potentially negative items to think about and plan for, it’s important to recognize that none of them are guaranteed to happen to you. In fact, your personal experience may be nothing but positive. That said, there’s likely some merit to that age-old planning advice, “Plan for the worst and hope for the best.” After all, the more prepared you are for potential obstacles, the more likely you are to be able to get past them.

3

Resources

Employment-related tools and support:

Entrepreneurial tools and support:

Recent Blogs

Disaster Preparedness: A Military Spouse’s Financial Readiness Guide

National Preparedness Month is a crucial reminder of the potential impact of both natural and man-made disasters. As a military spouse with frequent moves, you’ll want to know the risks at each duty station and update your plan accordingly. While we hope for the best, being prepared financially can significantly mitigate the stress and hardship…

Military Consumer Month: Smart Shopping for Military Spouse

Military Consumer Month: Smart Shopping for Military Spouses Feeling empowered to make smart money moves is critical year-round, but this Military Consumer Month is dedicated to raising awareness of the importance of savvy purchasing decisions and maximizing your hard-earned money. The month isn’t just about consumer protections and avoiding scams; it’s about making conscious choices…

Protect Your Belongings: The Importance of Insurance During a Military Move

Moving is a significant part of military life and let’s face it, packing up your cherished belongings and watching them ride off to your new location can sometimes be unsettling. One way to ease the stress of potential missing or damaged items is having adequate insurance. These simple steps can help you understand the value…

Honoring the Heart of Our Military: The Resilient Spouses

Military spouses are the unsung heroes of our military community. Their unwavering dedication, resilience and incredible adaptability are the backbone of our military families and communities. Military spouses manage households, raise families, often pursue careers or volunteer tirelessly, all while navigating the unique challenges of military life — frequent moves, deployments, and the emotional toll…

Giving Military Kids the Tools to Be Financially Capable

Military families are known for resilience, yet the frequent moves, deployments, and changes in income that come with military life can make financial stability feel like a juggling act. But these unique challenges may offer a golden teaching opportunity for military kids. By talking about finances openly and equipping kids with financial skills early on,…

March Money Moves: Navigating Tax Season While Preparing for Summer Fun

As we welcome the arrival of spring and the promise of warmer weather, it’s easy to get caught up in thoughts of summer plans and family vacations. But with tax season in full swing, it’s important to balance excitement for the upcoming months with a push to wrap up tax season. While those topics couldn’t…

Communicating with Your Partner About Finances: A February Focus on Financial Wellness

Talking Money with Your Partner As we celebrate loving relationships this month, it’s important to remember that not all conversations come up roses between couples. Sometimes discussing finances can be tricky and stir up negative emotions. Open communication about money is vital for building trust and nurturing a healthy relationship. Whether you’re a new couple…

Build Financial Wellness from the Ground Up in 2025

There’s something magical about the ball dropping at midnight and turning the page to a new year. For an instant, it feels like you’ve got a clean slate, and anything is possible. In some ways that’s true, but as the calendar page turns, your responsibilities, bills and financial challenges remain. Many people make resolutions to…