Using Credit Wisely

As a Financial Tool, Credit...

- Allows you to pay for things you could not afford with cash, such as a college education, new vehicle, or your first home.

- Helps you build a credit reputation — summarized in a credit report — that employers, landlords, future lenders, and other businesses often consider as they make decisions about you.

- Can also be dangerous if misused. Some individuals falsely view credit as a license to spend. In addition, poor spending habits can leave them deeply in debt and damage their credit reputation for years to come. Begin your journey to understand credit by clicking the button below.

Using Credit Wisely

As a Financial Tool, Credit...

- Allows you to pay for things you could not afford with cash, such as a college education, new vehicle, or your first home.

- Helps you build a credit reputation — summarized in a credit report — that employers, landlords, future lenders, and other businesses often consider as they make decisions about you.

- Can also be dangerous if misused. Some individuals falsely view credit as a license to spend. In addition, poor spending habits can leave them deeply in debt and damage their credit reputation for years to come. Begin your journey to understand credit by reading the four tips below.

Understand Credit

Practice Healthy Credit Habits

Using credit responsibly can help boost your overall financial well-being. Here are some tips to establish a healthy credit reputation:

- Set up and follow a budget so you don't accidentally run up debt.

- Pay bills on time. Do not skip payments.

- Pay off credit cards in full each month. If you must carry a balance, keep it as low as possible.

- Do not apply for credit you do not need.

- Keep credit card and loan information in a safe secure place to reduce the risk of identity theft.

- Keep your receipts and compare charges when your billing statements arrive. Call your company immediately if there is a discrepancy.

Monitor Your Credit Report

Your credit report is a record of your payment history with creditors. It is this report that employers, lenders, landlords, insurers and other businesses often evaluate to make decisions about your creditworthiness.

It shows the following:

- How much credit you are using

- How well you pay your debts

- Who is inquiring about your credit

- Information on bankruptcies or federal income tax liens

You can request your free annual credit report through the Annual Credit Report Request Service, a centralized contact point created by the three nationwide consumer reporting agencies: Equifax, Experian and TransUnion. Review your credit report annually for accuracy and any changes that may indicate fraudulent activity.

Many members of the military now have access to free electronic credit monitoring which may alert you to mistakes or problems with a credit report stemming from unauthorized use. Click on the "Free Credit Monitoring" PDF below for more information.

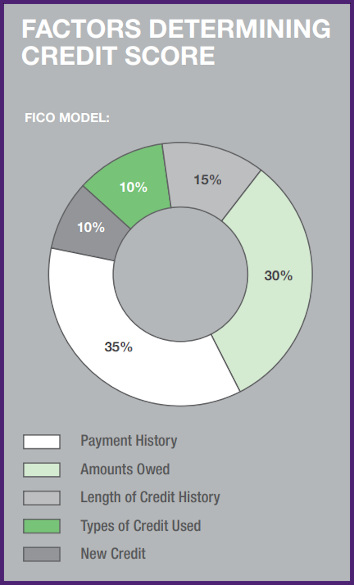

In reviewing your credit score, if it is high enough, you may qualify for the best rate on a loan or credit card account. A low score may cause you to be denied credit. Depending on the credit scoring model, scores may range from 300 to 850. Most lenders consider scores above 660 to be a good credit risk, while scores below 600 may indicate credit problems.

No single factor determines your score. But one or more of the factors may affect the final score more than others, depending on the overall information in your credit report.

Your score today could be different from your score three months from now. Ordering a copy of your own credit report or credit score does not impact your score.

Lenders use different credit scoring models depending on the type of credit for which you are applying. Still, you can obtain an educational score from any number of sources (sometimes for a fee) to give you a directional snapshot.

Choosing a Credit Card

Credit cards get a lot of people into deep financial trouble. However, if you use them well, credit cards can also have a positive impact on your financial life. Here are some guidelines to keep in mind if you open a credit card account:

- Minimize Rates and Fees: Search for a card with no annual fee and low interest rates. Beware of low introductory rates that balloon after a time. Always check the rates of competing credit card companies. There may be a better option for you in the long run.

- Always Have a Plan: Even though it doesn't take much thought to simply reach for your card and pay for things, don't ever use your card without thinking first.

- Avoid Cash Advances: Most credit cards charge high interest on cash advances as soon as they post to your account. It's best to avoid using this feature.

Finally, don't use a credit card as a license to spend now and pay later. Credit cards should typically be used for convenience and safety. Avoid the temptation to spend money you don’t have.

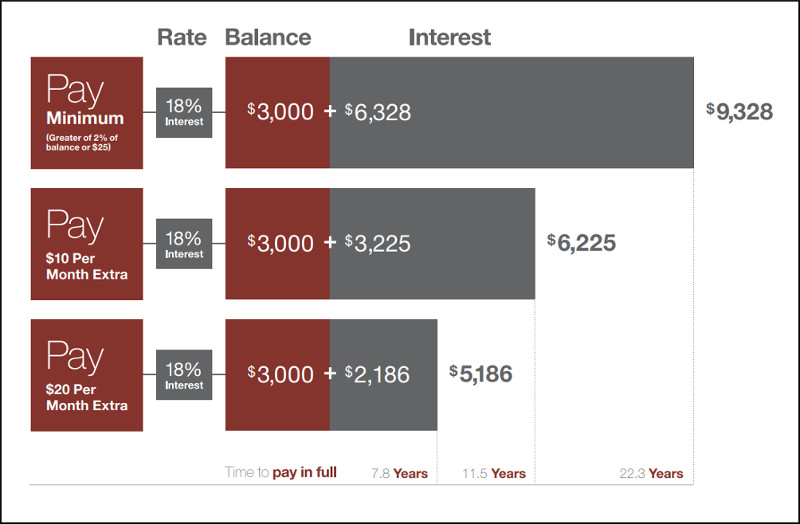

Paying the Minimum Is Costly

Try to pay more than the minimum. In the following illustration, paying the minimum each month will take approximately 22 years to pay off the balance. In fact, it will actually cost you more than twice the original charge. Increasing what you pay by as little as $10 or $20 each month will make a huge difference. Just by paying a little more each month, you can save thousands of dollars in interest costs and cut years off your repayment time. To understand credit even better, analyze the chart below.

MilLife Milestones

Watch

Dig Deeper

Understand Credit

Practice Healthy Credit Habits

Using credit responsibly can help boost your overall financial well-being. Here are some tips to establish a healthy credit reputation:

- Set up and follow a budget so you don't accidentally run up debt.

- Pay bills on time. Do not skip payments.

- Pay off credit cards in full each month. If you must carry a balance, keep it as low as possible.

- Do not apply for credit you do not need.

- Keep credit card and loan information in a safe secure place to reduce the risk of identity theft.

- Keep your receipts and compare charges when your billing statements arrive. Call your company immediately if there is a discrepancy.

Monitor Your Credit Report

Your credit report is a record of your payment history with creditors. It is this report that employers, lenders, landlords, insurers and other businesses often evaluate to make decisions about your creditworthiness.

It shows the following:

- How much credit you are using

- How well you pay your debts

- Who is inquiring about your credit

- Information on bankruptcies or federal income tax liens

You can request your free annual credit report through the Annual Credit Report Request Service, a centralized contact point created by the three nationwide consumer reporting agencies: Equifax, Experian and TransUnion. Review your credit report annually for accuracy and any changes that may indicate fraudulent activity.

Many members of the military now have access to free electronic credit monitoring which may alert you to mistakes or problems with a credit report stemming from unauthorized use.

In reviewing your credit score, if it is high enough, you may qualify for the best rate on a loan or credit card account. A low score may cause you to be denied credit. Depending on the credit scoring model, scores may range from 300 to 850. Most lenders consider scores above 660 to be a good credit risk, while scores below 600 may indicate credit problems.

No single factor determines your score. But one or more of the factors may affect the final score more than others, depending on the overall information in your credit report.

Your score today could be different from your score three months from now. Ordering a copy of your own credit report or credit score does not impact your score.

Lenders use different credit scoring models depending on the type of credit for which you are applying. Still, you can obtain an educational score from any number of sources (sometimes for a fee) to give you a directional snapshot.

Choosing a Credit Card

Credit cards get a lot of people into deep financial trouble. However, if you use them well, credit cards can also have a positive impact on your financial life. Here are some guidelines to keep in mind if you open a credit card account:

- Minimize Rates and Fees: Search for a card with no annual fee and low interest rates. Beware of low introductory rates that balloon after a time. Always check the rates of competing credit card companies. There may be a better option for you in the long run.

- Always Have a Plan: Even though it doesn't take much thought to simply reach for your card and pay for things, don't ever use your card without thinking first.

- Avoid Cash Advances: Most credit cards charge high interest on cash advances as soon as they post to your account. It's best to avoid using this feature.

Finally, don't use a credit card as a license to spend now and pay later. Credit cards should typically be used for convenience and safety. Avoid the temptation to spend money you don’t have.

Paying the Minimum Is Costly

Try to pay more than the minimum. In the following illustration, paying the minimum each month will take approximately 22 years to pay off the balance. In fact, it will actually cost you more than twice the original charge. Increasing what you pay by as little as $10 or $20 each month will make a huge difference. Just by paying a little more each month, you can save thousands of dollars in interest costs and cut years off your repayment time. To understand credit even better, analyze the chart below.

MilLife Milestones

Watch

Dig Deeper

Recent Blogs

Disaster Preparedness: A Military Spouse’s Financial Readiness Guide

National Preparedness Month is a crucial reminder of the potential impact of both natural and man-made disasters. As a military spouse with frequent moves, you’ll want to know the risks at each duty station and update your plan accordingly. While we hope for the best, being prepared financially can significantly mitigate the stress and hardship…

Military Consumer Month: Smart Shopping for Military Spouse

Military Consumer Month: Smart Shopping for Military Spouses Feeling empowered to make smart money moves is critical year-round, but this Military Consumer Month is dedicated to raising awareness of the importance of savvy purchasing decisions and maximizing your hard-earned money. The month isn’t just about consumer protections and avoiding scams; it’s about making conscious choices…

Protect Your Belongings: The Importance of Insurance During a Military Move

Moving is a significant part of military life and let’s face it, packing up your cherished belongings and watching them ride off to your new location can sometimes be unsettling. One way to ease the stress of potential missing or damaged items is having adequate insurance. These simple steps can help you understand the value…

Honoring the Heart of Our Military: The Resilient Spouses

Military spouses are the unsung heroes of our military community. Their unwavering dedication, resilience and incredible adaptability are the backbone of our military families and communities. Military spouses manage households, raise families, often pursue careers or volunteer tirelessly, all while navigating the unique challenges of military life — frequent moves, deployments, and the emotional toll…

Giving Military Kids the Tools to Be Financially Capable

Military families are known for resilience, yet the frequent moves, deployments, and changes in income that come with military life can make financial stability feel like a juggling act. But these unique challenges may offer a golden teaching opportunity for military kids. By talking about finances openly and equipping kids with financial skills early on,…

March Money Moves: Navigating Tax Season While Preparing for Summer Fun

As we welcome the arrival of spring and the promise of warmer weather, it’s easy to get caught up in thoughts of summer plans and family vacations. But with tax season in full swing, it’s important to balance excitement for the upcoming months with a push to wrap up tax season. While those topics couldn’t…

Communicating with Your Partner About Finances: A February Focus on Financial Wellness

Talking Money with Your Partner As we celebrate loving relationships this month, it’s important to remember that not all conversations come up roses between couples. Sometimes discussing finances can be tricky and stir up negative emotions. Open communication about money is vital for building trust and nurturing a healthy relationship. Whether you’re a new couple…

Build Financial Wellness from the Ground Up in 2025

There’s something magical about the ball dropping at midnight and turning the page to a new year. For an instant, it feels like you’ve got a clean slate, and anything is possible. In some ways that’s true, but as the calendar page turns, your responsibilities, bills and financial challenges remain. Many people make resolutions to…